Map : Gangnam |The Bubble That Never Burst

For thirty years, every serious economist called Gangnam a bubble. For thirty years, they were wrong. This is the story of why — and what it tells us about the next thirty.

B. Sun | Seoul Inside | May 2026

There Is a Post

There is a type of argument that recurs in every generation of Korean financial commentary, reliable as monsoon season. It goes like this: Gangnam apartment prices have detached from economic reality. The ratio of price to income is unsustainable. A correction is coming. Serious people — economists, central bankers, IMF analysts — have said versions of this sentence in 1991, in 2003, in 2008, in 2017, and again in 2023.

They were not stupid people. Their models were not wrong, exactly. The inputs were real: debt-to-income ratios genuinely alarming, price-to-rent ratios genuinely stretched, speculative demand genuinely present. In any textbook, these conditions precede a crash.

Gangnam did not crash.

What Gangnam did, over thirty years, was this:

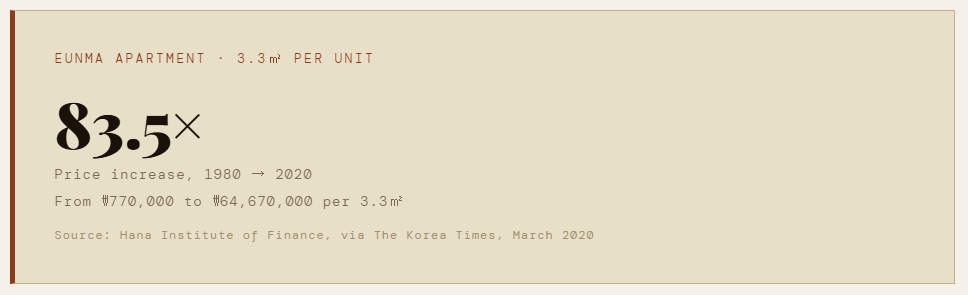

For comparison, the price of 4 kilograms of rice rose 3.2 times over the same period. Chicken rose 3.3 times. Gangnam apartments: 83.5 times.

This essay is about why that happened. More precisely, it is about the difference between a bubble and a structural truth — and why confusing the two has cost several generations of Koreans dearly.

02

The Definition of a Bubble, and Why It Matters

A bubble, in the formal economic sense, requires one thing above all else: it must burst. This is not a stylistic preference. It is definitional. Robert Shiller, who won the Nobel Prize partly for his work on asset price bubbles, describes the phenomenon as a “social epidemic” of price expectations that ends in a crash. Charles Kindleberger, whose Manias, Panics, and Crashes remains the standard text on the subject, writes of prices that diverge from intrinsic value to a degree that is “unsustainable” — meaning they return, eventually, to earth.

The word “unsustainable” is doing enormous work in that sentence. It is a prediction. And predictions require time horizons.

“A broken clock is right twice a day. A clock that has been wrong for thirty years is not a broken clock. It is a wall decoration.”

If an analyst in 1991 called Gangnam a bubble and the price corrected by 30% over the next three years and then rose 600% over the following twenty-five — did the bubble burst? The answer depends entirely on your time frame. On a three-year horizon: yes, something bubble-like occurred. On a thirty-year horizon: no. The 1991 peak was not a ceiling. It was a plateau on the way to a much higher place.

This is not a semantic game. It has real consequences. Every person who sold their Gangnam apartment in 1992 because “the bubble is bursting” and did not buy back watched their decision compound against them for three decades. The bubble call was directionally correct for approximately eighteen months. It was catastrophically wrong as a long-term thesis.

03

The First Spike — and Why It Didn’t Finish the Job

Between 1987 and 1989, Korean housing prices rose 30 to 40 percent per year. This is not gradual appreciation. This is the kind of number that appears in bubble postmortems. The proximate causes were a classic cocktail: Korea’s “3저 호황“ — the three-low boom of weak dollar, low oil prices, and low interest rates — combined with a severe housing shortage in Seoul and the psychological afterglow of the 1988 Olympics.

By 1991, prices had reached a level that genuinely could not be supported by organic demand. The correction came. Gangnam apartment prices fell — estimates vary, but a meaningful decline of 20 to 40 percent from peak was common across the mid-tier market. People who had bought near the top experienced real losses. The analysis that called this a bubble appeared, briefly, to be vindicated.

Then the government did something.

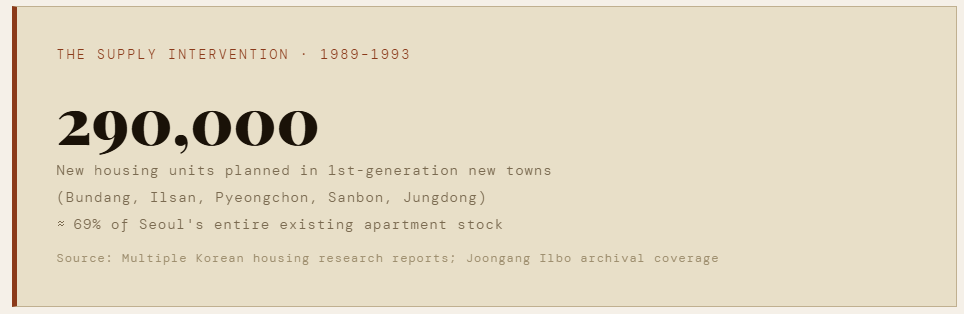

In April 1989, the Roh Tae-woo government announced one of the most aggressive housing supply programs in Korean history. Five new cities — the 1기 신도시 — would be built outside Seoul. Bundang to the south. Ilsan to the north. Together with three smaller sites, they would deliver 290,000 units — equivalent to nearly 70 percent of Seoul’s existing apartment stock — within three to four years.

Bundang’s first residents moved in during September 1991. Ilsan followed in 1992 and 1993. The supply shock was real. Gangnam prices, which had already begun to fall from their 1990-1991 peak, stayed suppressed through most of the decade.

Source: Citizens’ Coalition for Economic Justice (경실련) analysis; KB Real Estate price data

For most of the 1990s, Gangnam prices sat between ₩2.2 billion and ₩3 billion for a standard 30-pyeong unit. The supply intervention worked — for a decade. Then demand reasserted itself, interest rates fell again in the early 2000s, and the second great spike began.

Bundang, which had been built to relieve pressure on Gangnam, became “quasi-Gangnam” — absorbed into the premium orbit of the southern corridor. Ilsan, positioned near the northern suburbs, diverged: by 2020, a 32-pyeong Ilsan apartment that had sold for the same price as its Bundang equivalent in 1990 was worth ₩5 billion. The Bundang equivalent: ₩8.3 billion.

Same policy. Same entry price. Thirty years: completely different outcomes determined by one variable — proximity to the center.

04

The Fifteen-Year Rhythm

The Korea Times piece that documented the 83.5× price increase noted something that deserves more attention than it received: Gangnam prices have not risen smoothly. They have risen in three distinct spikes, each approximately fifteen years apart.

1988 — 1991

First spike. The three-low boom. Olympic afterglow. Severe housing shortage. Prices surge 30–40% per year. Government responds with 1기 신도시. Prices correct and stay suppressed for most of the decade.

2002 — 2005

Second spike. Low interest rates sustained after the Asian financial crisis recovery. Household lending grows. The generation that was priced out in the 1990s now has income and credit. Gangnam reasserts its premium.

2018 — 2020

Third spike. Moon Jae-in administration’s demand-suppression policies — intended to cool the market — paradoxically signal scarcity, concentrate demand in core areas, and accelerate the premium in the very neighborhoods they were meant to restrain.

Three spikes. Three corrections. And after each correction: a new, higher floor. The 1991 peak became the 1999 floor. The 2005 peak became the 2012 floor. Each generation of buyers who “waited for the correction” found that the correction, when it came, did not return prices to where they had entered. It returned them to a level that was still above where the previous generation had bought.

This is not a bubble. A bubble returns to its origin. This is a staircase.

05

Five Hundred Years of the Same Problem

Here is the part that the economic models miss entirely, because it cannot be entered into a spreadsheet.

Korea has had one dominant city for over five centuries. It has been called Hanyang, then Gyeongseong, then Seoul. The name has changed. The logic has not. In a country organized around a single capital — culturally, politically, economically, educationally — the premium attached to living near the center is not a market distortion. It is the market expressing a permanent structural reality.

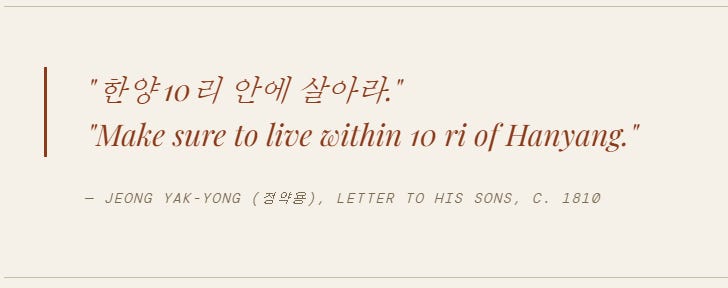

Jeong Yak-yong — Dasan — is one of the most revered scholars in Korean history. His portrait has appeared on the 1,000-won note. He spent nearly two decades in exile in the southern province of Jeolla. When he wrote to his sons from exile around 1810, his advice was blunt and specific: “한양 10리 안에 살아라.” Live within 10 ri — roughly four kilometers — of the capital.

The logic was not sentimental. It was structural. In Joseon Korea, as in modern Korea, opportunity, information, political networks, and social mobility were concentrated in the capital. To leave was to accept permanent downward mobility. The geography of advantage had a precise address.

Yi Hwang — Toegye — whose portrait graces the 1,000-won bill, rented his home in Hanyang for most of his career. The word he used in his own collected works — 임옥 (賃屋), literally “a house rented for payment” — is not a metaphor. Korea’s greatest Confucian scholar could not afford to buy in the capital city he needed to be in.

By 1754, the housing shortage had become acute enough that the Joseon royal government — the Hanseongbu — identified and punished more than twenty aristocrats at once for simply seizing civilian homes by force. King Yeongjo issued a compromise: officials could rent the outer wing of civilian homes, on a limited basis, because there was nowhere else for them to live.

Regulate. Crack down. Quietly walk it back because the supply problem was never solved. The governance response to Seoul’s housing crisis, in 1754, would be recognizable to anyone who has followed the last thirty years of Korean real estate policy.

The structural conditions — one dominant city, chronic undersupply, severe information asymmetry, concentrated opportunity — have produced the same outcome across five centuries: housing in the capital is expensive beyond what most incomes can support, and it keeps getting more expensive.

This is not a bubble. This is the oldest story in Korean economic history.

06

What “Bubble” Was Actually Describing

The analysts who called Gangnam a bubble were not wrong about what they observed. They observed speculative demand — people buying apartments not to live in them but to sell them. They observed leverage — buyers taking on debt that their incomes could not comfortably service. They observed psychological contagion — the belief that prices would rise forever, spreading through social networks and changing behavior.

All of this was real. Edward Chancellor, whose Devil Take the Hindmost remains the definitive history of financial speculation, would recognize every element. The crowd psychology. The leverage. The “this time is different” mentality that arrives reliably at every peak.

But Chancellor’s framework also contains a crucial variable that the Gangnam analysts underweighted: supply elasticity. In markets where supply can respond to demand — where high prices attract new construction that eventually equilibrates the market — bubbles do burst. The new supply arrives, prices fall, the speculators are ruined.

Gangnam’s supply is not elastic. It cannot be. The geography is fixed. The political economy of Korean urban development has made large-scale densification in the core nearly impossible for decades. The 1기 신도시 worked precisely because it created genuine alternatives — for a while. When those alternatives were absorbed into the premium orbit, the pressure returned to the center.

What the bubble analysts were describing was real speculative behavior layered on top of a structural scarcity. They correctly identified the speculative layer. They incorrectly assumed that the structural layer would behave like a normal market. It didn’t. It doesn’t. It won’t, as long as Korea remains organized around one dominant city.

Source: Korean academic research, 2026; cited in multiple policy analyses

07

The Cost of Being Wrong About This

The bubble thesis has not been merely incorrect. It has been costly — specifically and measurably costly — to the people who believed it.

Consider the arithmetic of 1993. A 30-pyeong Gangnam apartment was available for approximately ₩220 million. Someone who had watched the 1988-1991 spike, seen the correction, concluded “the bubble has burst, prices will normalize” and chose not to buy — that person watched the same apartment reach ₩2.1 billion by 2020. Not a recovery. Not a return to trend. An increase of nearly 10× from the post-correction floor.

The lost decade argument — that buyers in the late 1980s peak suffered for years — is true. It is also, in the thirty-year view, irrelevant. The buyers at the 1991 peak, who endured the worst of the correction, nonetheless ended up dramatically wealthier than the non-buyers who congratulated themselves on their patience.

This asymmetry — between the cost of being wrong about a bubble in a structurally scarce market versus the cost of being wrong about a bubble in a genuinely elastic market — is the central analytical error of a generation of Korean real estate commentary.

The Lesson That Keeps Not Being Learned

Each of the three spikes has produced the same cycle. Prices rise beyond any defensible income-based valuation. Serious people call it a bubble. There is a correction — real, painful, lasting two to four years. The serious people feel vindicated. Then prices resume their structural ascent, and the floor is higher than the previous cycle’s peak.

After 1991: the serious people were right for three years. Then wrong for twenty-five.

After 2008: the serious people were right for two years. Then wrong again.

The pattern is consistent enough that it has a name in Korean investment circles. It doesn’t need to be printed here. Anyone who has watched Korean real estate for more than a decade knows exactly what it is.

08

What Thirty Years From Now Will Look Like

This essay will be wrong about something. All essays written about living markets are wrong about something, eventually. The honest question is: wrong about what, and in which direction?

The structural conditions that have driven Gangnam’s price appreciation for five centuries — and measurably for the last forty years — have not changed. Korea remains organized around one dominant city. The political economy of Korean urban development remains resistant to the kind of densification that would meaningfully increase core supply. The educational, cultural, and economic networks that make proximity to the center valuable continue to generate premium demand.

What has changed, or is changing:

Demographics. Korea’s fertility rate is the lowest of any country in recorded history. The population is declining. At some point — not immediately, but eventually — this will reduce the absolute number of households competing for Seoul real estate. When that point arrives, the structural scarcity argument weakens.

Remote work and infrastructure. High-speed rail and remote work have begun, slowly, to redistribute the geography of opportunity. If Dasan’s “10 ri rule” becomes less structurally binding — if proximity to the center matters less — the premium attached to centrality will compress.

Policy. The history of Korean real estate policy is a history of interventions that consistently failed to address supply and consistently addressed demand instead, with predictable effects. If this changes — genuinely changes, not rhetorically changes — the structural dynamic changes with it.

None of these are imminent. None of them are certain. But they are the conditions under which the five-century structural argument finally breaks. Not a bubble bursting. A structure slowly dissolving.

The question is not “when will the bubble burst?” The bubble already burst, in 1991, and again in 2008, and prices recovered both times. The correct question is: “when do the structural conditions change?” That is a different question with a different answer.

09

Dasan’s Letter, Reread

Jeong Yak-yong wrote to his sons from exile. He had been sent away from the capital — stripped of office, separated from the networks that made a career possible in Joseon Korea. His advice was not about real estate. It was about proximity to power, to information, to the social infrastructure of a society organized around a single dominant city.

한양 10리 안에 살아라.

He was not saying: buy in Hanyang because prices will rise. He was saying: the geography of opportunity in this country has a specific address, and distance from that address compounds against you every year.

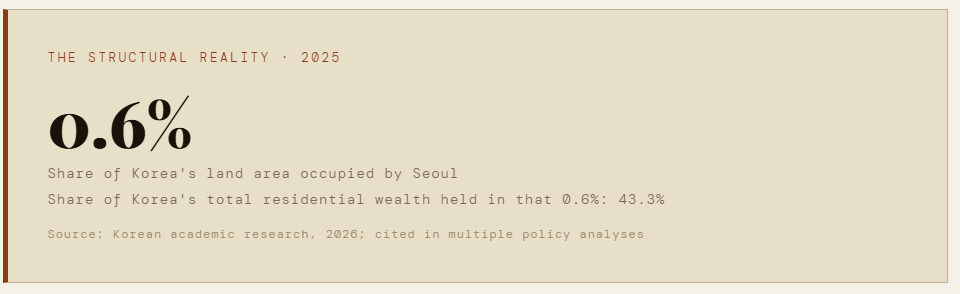

Two hundred and sixteen years later, the Seoul Metropolitan Government’s own data shows that 43.3% of Korea’s residential wealth is concentrated in 0.6% of the country’s land area. The address has changed. The logic has not.

Whether that is right or wrong — whether it reflects a healthy society or a deeply distorted one — is a separate question, and an important one. Korea’s housing crisis is real. The pain of the priced-out generation is real. The social consequences of concentrating this much wealth in this small an area are real and serious.

But “real and serious” is not the same as “about to correct.” Serious structural distortions can persist for a very long time. In this case, the evidence suggests: approximately five hundred years and counting.

The bubble that never burst was never a bubble. It was a mirror — reflecting, with uncomfortable accuracy, the way Korea has organized itself for half a millennium.

Dasan knew. He just couldn’t afford to live there either.

“고장난 시계도 하루에 두 번은 맞는다.

30년간 한 번도 맞지 않은 시계는

고장난 시계가 아니다.

그것은 벽에 그려진 그림이다.”

A broken clock is right twice a day.

A clock wrong for thirty years is not broken.

It is a painting on a wall.

Seoul Inside · B. Sun · May 2026

Sources & Verification

83.5× price increase (Eunma Apartment, 1980–2020): Hana Institute of Finance data, reported in Kim Bo-eun, “Gangnam apartment prices jump 84 times in 40 years,” The Korea Times, March 2020. koreatimes.co.kr

Three-low boom / 30–40% annual price surge 1987–1989: Multiple Korean housing research reports; consistent across academic and media sources covering the period.

1기 신도시 — 290,000 units / 69% of Seoul stock: Korean housing policy research; Joongang Ilbo archival coverage of the 1989 announcement.

Gangnam 30-pyeong price data (1993 / 1999 / 2020): Citizens’ Coalition for Economic Justice (경실련) analysis; KB Real Estate historical price data. Reported in Moneytimes and related outlets.

Bundang vs. Ilsan 2020 price comparison: Joongang Ilbo, “1990년 같은 5800만원 일산·분당 아파트…지금은 5억·8억3000만원 천양지차.” joongang.co.kr

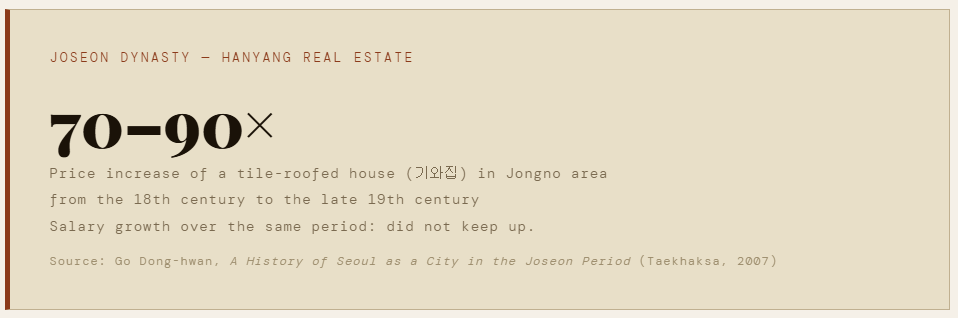

Joseon housing price data (70–90× over one century): Go Dong-hwan, A History of Seoul as a City in the Joseon Period (Taekhaksa, 2007).

Dasan’s letter / “한양 10리 안에 살아라”: Dasan Simunjip (다산시문집). db.itkc.or.kr

Yi Hwang / 임옥 (rented house): Toegye Seonsaeng Munjip (퇴계선생문집), Vol. 2. db.itkc.or.kr

1754 Hanseongbu crackdown on aristocratic squatting: Annals of King Yeongjo (영조실록). sillok.history.go.kr

0.6% land / 43.3% wealth concentration: Korean academic research, 2026. Cited in policy analyses reviewed for this essay.

This essay draws on and extends themes first explored in “Seoul Real Estate Has Always Been Unaffordable — Even 500 Years Ago,” Seoul Inside, May 2026. Readers interested in the Joseon primary sources are directed to that piece for full citation detail.

https://seoulinside.substack.com/p/koreas-only-true-bubble-and-why-it

https://seoulinside.substack.com/p/the-bubble-that-never-burst

https://seoulinside.substack.com/p/the-trickle-dry-effect

https://seoulinside.substack.com/p/the-rubber-ruler-problem

https://seoulinside.substack.com/p/stacking-of-infrastructure-a-prologue

https://seoulinside.substack.com/p/urban-layer-stacking-how-cities-survive